Navigating the complexities of tax deductions can feel like deciphering a secret code. But what if we told you that you might be leaving money on the table by overlooking a potentially significant deduction: your health insurance premiums? This guide unravels the intricacies of claiming this deduction, clarifying the eligibility criteria, outlining the necessary documentation, and highlighting common pitfalls to avoid. Whether you’re self-employed or employed, understanding these rules can significantly impact your tax liability.

This guide will walk you through the process of determining whether you can deduct your health insurance premiums, explaining the differences between deductions for employees and the self-employed, the role of Health Savings Accounts (HSAs), and the proper documentation required for filing your taxes. We’ll provide clear examples and address common misunderstandings to empower you to confidently claim your rightful deduction.

Eligibility for Deduction

Deductibility of health insurance premiums hinges on several factors, primarily your employment status and the type of health insurance plan. Understanding these criteria is crucial for accurately filing your taxes and claiming eligible deductions. The rules differ significantly between employees and self-employed individuals.

Deduction Criteria for Health Insurance Premiums

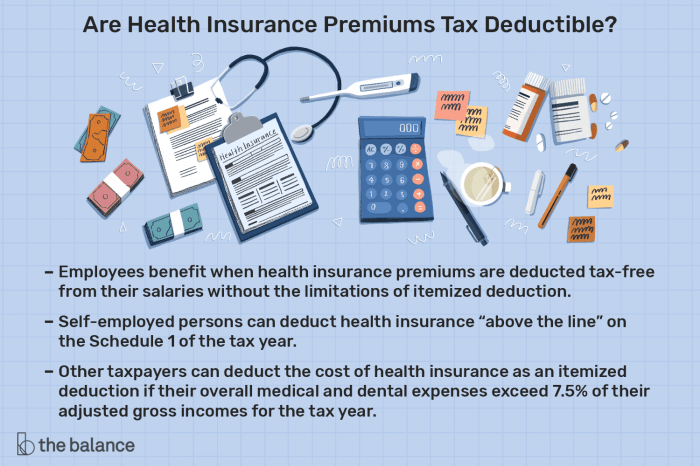

To deduct health insurance premiums, you must have paid premiums for health insurance coverage that meets specific requirements. Generally, the plan must provide medical care benefits, and the premiums must be for medical insurance, not supplemental insurance like dental or vision (unless bundled as part of a qualifying medical plan). The premiums must be for you, your spouse, and/or your dependents. You cannot deduct premiums paid for insurance that covers only long-term care or accident insurance. The IRS provides specific guidelines on what constitutes a qualifying health insurance plan.

Deduction Requirements for Self-Employed Individuals

Self-employed individuals can deduct the amount they paid in health insurance premiums as an above-the-line deduction. This means the deduction is made before calculating adjusted gross income (AGI), resulting in a larger deduction than itemized deductions for many. To claim this deduction, you must be self-employed or a freelancer and itemize your deductions on Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship). You must also have reported your business income and expenses accurately. Crucially, you cannot be eligible for employer-sponsored health insurance.

Comparison of Deduction Rules for Employees and Self-Employed Individuals

Employees typically cannot deduct health insurance premiums if they are covered by an employer-sponsored plan. This is because the employer often contributes to the cost of the insurance, and the employee’s portion is considered a pre-tax deduction from their salary. However, if an employee is uninsured and pays for their own health insurance, they might be able to deduct medical expenses exceeding 7.5% of their adjusted gross income (AGI), but this is different from deducting the premiums directly. Self-employed individuals, on the other hand, can deduct their health insurance premiums directly, provided they meet the criteria Artikeld above. This difference arises from the fundamental difference in how employment income and self-employment income are treated for tax purposes.

Examples of Qualifying Health Insurance Plans

Qualifying health insurance plans typically include plans offered through the Health Insurance Marketplace (healthcare.gov), plans purchased directly from private insurance companies, and plans offered through professional associations or unions. Medicare and Medicaid are generally not eligible for premium deductions. Specific plans vary widely in coverage and cost. A specific example could be a policy from Blue Cross Blue Shield or UnitedHealthcare, provided it meets the IRS’s definition of a qualifying health insurance plan. The key is that the plan must provide comprehensive medical care benefits.

Eligibility Based on Employment Status and Plan Type

| Employment Status | Plan Type | Deductible Premiums? | Notes |

|---|---|---|---|

| Employee (Employer-sponsored plan) | Employer-provided | No | Premiums are generally not deductible; employer contributions are considered pre-tax compensation. |

| Employee (No employer-sponsored plan) | Individually purchased | Potentially (Medical Expense Deduction) | Only deductible if medical expenses exceed 7.5% of AGI. |

| Self-Employed | Individually purchased | Yes | Premiums are deductible as an above-the-line deduction. |

| Self-Employed | Employer-provided (as an employee of another business) | No | Same rules as for employees apply. |

Types of Health Insurance Premiums Deductible

Understanding which health insurance premiums are deductible can significantly impact your tax liability. This section clarifies the types of premiums eligible for deduction, focusing on self-employed individuals and those without employer-sponsored plans, as these are the situations where premium deductibility is most relevant. The rules can be complex, so careful consideration is crucial.

Premiums paid for health insurance coverage are deductible for self-employed individuals and their families under certain circumstances. The deduction is taken above the line, meaning it reduces your adjusted gross income (AGI). This is a significant advantage compared to itemized deductions, which are subject to thresholds and limitations. The specific rules regarding deductibility depend on the type of plan and how the premiums are paid.

Deductibility of Premiums for Spouse and Dependents

Premiums paid for a taxpayer’s spouse and dependents are generally deductible as long as the taxpayer is self-employed or has no employer-sponsored health insurance. The deduction includes premiums for coverage under a qualifying health insurance plan. The IRS defines a dependent as a qualifying child or qualifying relative who meets specific criteria regarding age, residency, and financial support. Proper documentation supporting the dependency status is crucial for claiming the deduction. For example, if a self-employed individual covers their spouse and two children under their health insurance plan, the premiums for all four individuals are generally deductible.

Deductibility of Premiums Paid Through a Health Savings Account (HSA)

Premiums paid for a qualified health insurance plan using funds from a Health Savings Account (HSA) are not directly deductible. The contributions to the HSA itself are deductible, up to the annual contribution limit, but the money used from the HSA to pay for premiums is not deductible again. This is because the HSA contribution itself already provided a tax advantage. Think of it as a tax-advantaged savings account specifically for healthcare expenses; the funds within the HSA are already tax-free, so withdrawing them to pay premiums doesn’t generate another deduction.

Examples of Premiums That Are NOT Deductible

Not all health insurance premiums are deductible. Premiums paid through an employer-sponsored plan are generally not deductible, as the employer typically covers a portion of the cost. Similarly, premiums for long-term care insurance are usually not deductible, except under specific circumstances and with specific types of policies. Premiums for supplemental health insurance policies, such as dental or vision insurance, are also typically not deductible unless specifically included as part of a comprehensive health insurance plan. Medicare Part B premiums are not deductible, as are premiums for health insurance obtained through the Affordable Care Act (ACA) marketplaces when a taxpayer is eligible for employer-sponsored coverage.

Deductible and Non-Deductible Premium Types

The following list summarizes the key distinctions:

- Deductible: Premiums paid by self-employed individuals for themselves, their spouse, and their dependents under a qualified health insurance plan.

- Non-Deductible: Premiums paid through employer-sponsored plans; premiums for long-term care insurance (generally); premiums for supplemental health insurance (generally); Medicare Part B premiums; premiums for ACA marketplace plans when employer-sponsored coverage is available.

Tax Form and Documentation Requirements

Accurately reporting your health insurance premium deductions requires careful record-keeping and the correct completion of relevant tax forms. Understanding the necessary information and documentation will ensure a smooth and successful tax filing process. Failure to provide sufficient documentation can lead to delays or rejection of your claim.

The specific tax form and sections will vary depending on your country and tax system. In the United States, for example, you’ll primarily use Form 1040 and Schedule 1 (Additional Income and Adjustments to Income) to report these deductions. Other countries will have their own equivalent forms. Always refer to the most current instructions provided by your relevant tax authority.

Information Required for Reporting Health Insurance Premium Deductions

To successfully claim the deduction, you must provide comprehensive information about your health insurance premiums. This includes the total amount paid during the tax year, the name of the insurance provider, policy number, and the dates of coverage. For self-employed individuals, additional information might be required to verify eligibility.

Completing Relevant Sections on the Tax Form

The process of completing the relevant tax form sections involves accurately transferring the information from your supporting documentation. This typically includes entering the total amount of premiums paid in the designated area on Schedule 1. Carefully review the instructions accompanying the tax form to ensure you enter the data in the correct fields. Incorrect placement can result in processing errors. For example, on the US Form 1040 Schedule 1, you would typically report the total premiums paid in the appropriate line for medical expense deductions.

Examples of Acceptable Supporting Documentation

Acceptable documentation generally includes your insurance policy, premium payment receipts (bank statements, canceled checks, credit card statements, etc.), and any 1099-MISC forms received from your insurance provider detailing payments made. The documentation must clearly show the dates of coverage, the amount paid, and the payer and payee information. Digital copies are usually acceptable, provided they are legible and easily verifiable.

Step-by-Step Guide for Documenting Premium Payments

- Gather all documentation: Collect all statements, receipts, and policy information related to your health insurance premiums for the tax year.

- Organize documents chronologically: Arrange the documents by date, making it easier to review and verify payments.

- Create a spreadsheet (optional): For ease of summary and accuracy, create a spreadsheet listing each payment: date, amount, payment method, and a brief description.

- Total premium payments: Calculate the total amount of premiums paid during the tax year. This total will be entered on your tax form.

- Securely store documents: Keep all original documents in a safe place, organized and easily accessible for potential audits.

Organizing Tax Documents Related to Health Insurance

Proper organization is crucial for efficient tax preparation and potential audits. A dedicated file or folder for all health insurance-related tax documents is recommended. Consider using a system that allows for easy retrieval, such as a chronological filing system or a system organized by payer. Maintain digital copies as well for backup and easy access. Clearly label all files and folders for quick identification.

Self-Employment and Health Insurance Deductions

Self-employed individuals face unique challenges when it comes to securing health insurance and claiming deductions. Unlike employees who often have employer-sponsored plans, the self-employed must purchase their own coverage, making the ability to deduct premiums a crucial aspect of tax planning. Understanding the rules and potential pitfalls is essential for maximizing tax savings.

Self-employed individuals can deduct the amount they paid in health insurance premiums as an above-the-line deduction. This means the deduction is made before calculating adjusted gross income (AGI), resulting in a larger tax savings compared to itemized deductions, which are subtracted after AGI calculation. The process involves accurately tracking premium payments throughout the year and reporting them on the appropriate tax form.

Deduction Limits for Self-Employed Individuals

The self-employed can deduct the total amount of health insurance premiums paid for themselves, their spouse, and their dependents, provided they meet eligibility requirements (discussed previously). There is no upper limit on the amount deductible, unlike some other deductions. However, the deduction is limited to the amount of self-employment income reported. If health insurance premiums exceed self-employment income, only the amount up to the self-employment income is deductible. This contrasts with employees, who can deduct health insurance premiums only under certain circumstances (such as through a health savings account or if the employer doesn’t offer coverage), and those deductions may be subject to other limitations.

Impact of Other Deductions on Health Insurance Premium Deduction

Other deductions do not directly impact the amount of health insurance premiums you can deduct. The health insurance premium deduction is calculated separately. However, the overall tax liability is affected by all deductions. A higher total deduction, including the health insurance premium deduction, will lead to a lower taxable income and therefore lower overall tax. For example, deducting business expenses in addition to health insurance premiums will reduce your taxable income, resulting in greater savings, even if the health insurance deduction amount remains unchanged.

Common Mistakes When Claiming the Deduction

Several common errors can lead to missed deductions or even IRS penalties. One frequent mistake is failing to accurately track all premium payments throughout the year. Keeping detailed records, including receipts and payment confirmations, is crucial. Another common mistake involves incorrectly classifying expenses. Premiums paid for supplemental insurance or non-qualified health plans may not be deductible. Finally, some taxpayers mistakenly deduct premiums paid for dependents who are not eligible. Eligibility requirements must be carefully reviewed to avoid errors.

Claiming the Health Insurance Premium Deduction: A Flowchart

The following illustrates the process:

[Imagine a flowchart here. The flowchart would begin with a box labeled “Are you self-employed and paid health insurance premiums?” A “Yes” branch would lead to a box labeled “Track all premium payments and gather supporting documentation (receipts, statements).” This would lead to a box labeled “Determine your self-employment income.” A subsequent box would read “Calculate the deductible amount (the lesser of total premiums paid or self-employment income).” A “No” branch from the first box would lead to a terminal box labeled “You are not eligible for this specific deduction.”]

Epilogue

Successfully navigating the world of health insurance premium deductions requires careful attention to detail and a thorough understanding of the relevant regulations. While the process might seem daunting at first, armed with the knowledge presented in this guide, you can confidently determine your eligibility, gather the necessary documentation, and accurately report your deduction. Remember, taking the time to understand these rules can result in substantial tax savings, making it a worthwhile endeavor. Consult with a tax professional if you have specific questions or complex situations.

General Inquiries

Can I deduct premiums if I’m covered under my spouse’s plan?

Generally, no, unless you are self-employed and your spouse’s plan doesn’t cover you.

What if I only paid premiums for part of the year?

You can only deduct premiums for the months you were covered and paid premiums.

Are short-term health insurance premiums deductible?

No, short-term health insurance premiums are generally not deductible.

Where do I report health insurance premium deductions on my tax return?

The specific form and location will vary depending on your filing status and whether you are self-employed or an employee. Consult the IRS instructions for the relevant tax form.

What happens if I make a mistake on my tax return regarding this deduction?

You can file an amended tax return (Form 1040-X) to correct any errors. It’s advisable to consult a tax professional for guidance.