The financial landscape of insurance hinges on the consistent payment of premiums. While various payment schedules exist, paying insurance premiums annually presents a unique set of advantages and disadvantages for both the insured and the insurer. This exploration delves into the intricacies of annual premium payments, examining their impact on budgeting, financial planning, and the overall insurance ecosystem.

We will navigate the administrative processes involved, compare annual payments to other payment frequencies, and analyze how risk factors and policy specifics influence the final premium amount. Understanding the nuances of annual premium payments empowers individuals to make informed decisions about their insurance coverage and financial well-being.

Premium Payment Frequency

Choosing the right premium payment frequency significantly impacts both the insured and the insurer. While annual payments offer potential cost savings, other options provide greater flexibility. Understanding the advantages and disadvantages of each approach is crucial for informed decision-making.

Advantages and Disadvantages of Annual vs. Other Payment Schedules

Annual premium payments typically offer the lowest overall cost due to insurers often providing discounts for upfront payments. This reflects reduced administrative overhead and improved cash flow predictability for the insurer. However, this requires a significant upfront capital outlay for the insured, potentially creating a financial burden. Semi-annual, quarterly, and monthly payments offer greater flexibility, allowing for easier budgeting and smaller, more manageable payments. However, these options usually come with a higher overall premium cost due to added administrative expenses and the time value of money for the insurer. The convenience of smaller, more frequent payments must be weighed against the increased total cost.

Administrative Processes for Annual Premium Payments

Handling annual premium payments involves a streamlined process for insurance companies. Upon receipt of payment, the insurer verifies the payment amount and applies it to the policy. This process often involves automated systems for tracking payments, updating policy records, and generating receipts. Data entry and reconciliation are minimized compared to more frequent payment schedules, reducing administrative overhead and potential for errors. The insurer might also utilize various payment methods such as online portals, bank transfers, or mailed checks. Efficient processing of annual payments contributes to the insurer’s overall operational efficiency.

Impact of Payment Frequency on Insurer Cash Flow

Annual premium payments significantly benefit an insurer’s cash flow. Receiving a large sum upfront provides substantial liquidity, enabling the insurer to invest funds, meet operational expenses, and manage claims more effectively. This contrasts with more frequent payment schedules where cash inflow is more evenly distributed throughout the year, potentially impacting short-term liquidity. Predictable annual inflows reduce the need for short-term borrowing or reliance on other financial instruments to maintain operational solvency. The improved cash flow predictability allows for better financial planning and risk management for the insurer.

Comparison of Premium Costs Across Payment Frequencies

The following table illustrates how premium costs vary with payment frequency, including potential interest charges or discounts. These figures are illustrative and actual costs may vary depending on the insurer and specific policy.

| Payment Frequency | Annual Premium | Semi-Annual Premium | Quarterly Premium | Monthly Premium |

|---|---|---|---|---|

| Example Policy | $1200 (10% discount) | $660 | $330 | $110 |

| Another Example Policy | $2400 (5% discount) | $1260 | $630 | $210 |

| *Note:* Discounts shown are illustrative and vary widely based on insurer and policy type. More frequent payments may incur small additional fees. |

Impact of Annual Premiums on Insured

Paying insurance premiums annually presents a unique set of financial considerations for the insured. Understanding the implications of this payment schedule is crucial for effective budgeting and long-term financial planning. This section explores the effects of annual premium payments on an individual’s finances, weighing the advantages and disadvantages against more frequent payment options, and offering practical strategies for successful management.

Annual premium payments significantly impact an insured’s budgeting and financial planning. The most immediate effect is the need to allocate a larger sum of money at a single point in the year compared to spreading payments across several months. This requires careful budgeting and potentially adjusting spending in other areas to accommodate the premium payment. For example, a family might need to temporarily reduce discretionary spending in the months leading up to their annual insurance premium due date. This contrasts with monthly or quarterly payments, which allow for a more gradual and predictable outflow of funds. Failing to properly plan for this large annual expense can lead to financial strain and potential difficulty meeting other financial obligations.

Benefits and Drawbacks of Annual Premium Payments

Paying insurance premiums annually often comes with a discount, as insurers incentivize prompt and lump-sum payments. This discount can translate into significant savings over the course of a policy term, making annual payments a more cost-effective option for many individuals. However, the drawback is the need for a substantial upfront payment, which may cause financial difficulties for some. The potential for unexpected expenses or financial emergencies during the year further increases the risk associated with this approach. For example, an unexpected car repair or medical bill could severely impact an individual’s ability to meet their annual insurance premium. Conversely, more frequent payments offer better cash flow management but usually come with a higher overall cost due to the absence of the annual discount. The choice depends heavily on an individual’s financial situation and risk tolerance.

Strategies for Managing Annual Premium Payments

Effective management of annual premium payments requires proactive planning and resourcefulness. One effective strategy is setting up a dedicated savings account specifically for insurance premiums. Regular contributions throughout the year ensure sufficient funds are available when the premium is due. Another approach involves utilizing budgeting apps or spreadsheets to track income and expenses, allowing for precise allocation of funds towards the annual premium. For those with irregular income, exploring options like automatic bank transfers from savings or checking accounts can ensure consistent savings towards the premium payment. This proactive approach helps mitigate the financial strain of a large, single payment.

Resources for Managing Large Annual Insurance Payments

Individuals facing challenges in managing large annual insurance payments can leverage several resources. A well-structured budget is paramount, and many free online tools and templates can assist with this. Financial advisors can provide personalized guidance on managing finances and allocating funds for large expenses. Additionally, some insurance companies offer payment plans that allow for installment payments, though these may not offer the same discounts as annual payments.

- Online Budgeting Tools: Numerous free and paid online budgeting tools and apps (e.g., Mint, YNAB, Personal Capital) provide resources for creating and managing a budget effectively.

- Financial Advisors: Consulting a financial advisor can offer personalized advice on budgeting, saving, and investment strategies to manage large expenses like annual insurance premiums.

- Insurance Company Payment Plans: Contacting your insurance provider to inquire about payment plan options can help spread the cost over time, although it may come at a slightly higher overall cost.

- Credit Unions and Banks: Credit unions and banks often provide financial counseling and resources for managing personal finances.

Illustrative Example of Annual Premium Calculation

This section provides a hypothetical example to illustrate how an annual insurance premium is calculated. We will examine a simplified scenario to clarify the underlying principles. Understanding these principles allows for a better comprehension of how individual risk factors influence the final premium amount.

Let’s consider a hypothetical 30-year-old individual, Alex, applying for a comprehensive car insurance policy. Several factors will be used to determine Alex’s annual premium.

Assumptions and Risk Factors

The following assumptions underpin our premium calculation:

- Vehicle Type and Value: Alex drives a mid-range sedan valued at $25,000. More expensive vehicles generally attract higher premiums due to increased repair costs.

- Driving History: Alex has a clean driving record with no accidents or traffic violations in the past five years. A history of accidents or violations would increase the premium.

- Location: Alex resides in an area with a relatively low crime rate and fewer accidents. Higher-risk areas with increased theft or accident frequency lead to higher premiums.

- Coverage Level: Alex opts for comprehensive coverage, including liability, collision, and comprehensive protection. Higher coverage levels naturally result in higher premiums.

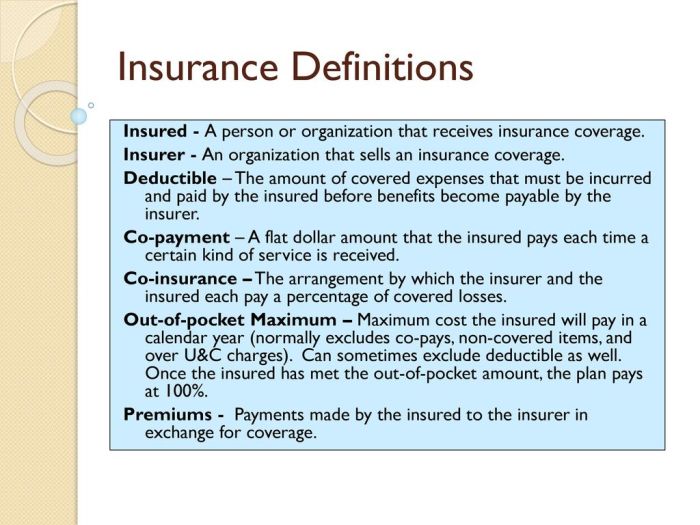

- Deductible: Alex chooses a $500 deductible. A higher deductible (the amount Alex pays before the insurance kicks in) lowers the premium, as the insurer’s financial risk is reduced.

Premium Calculation Process

A simplified representation of the premium calculation process is shown below. Note that actual calculations are far more complex and involve proprietary actuarial models.

Step 1: Base Premium

The insurer starts with a base premium for a standard policy based on the vehicle type and coverage level. Let’s assume this base premium is $800.

Step 2: Risk Factor Adjustments

Next, the base premium is adjusted based on Alex’s individual risk factors. For instance:

- Clean Driving Record: A discount of 15% is applied (reducing the premium by $120).

- Location: A small discount of 5% is applied (reducing the premium by $40).

- Deductible: A discount of 10% is applied (reducing the premium by $80).

Step 3: Final Annual Premium

The final annual premium is calculated by subtracting the discounts from the base premium:

$800 (Base) – $120 (Driving) – $40 (Location) – $80 (Deductible) = $560

Therefore, Alex’s annual premium is $560.

Impact of Risk Factor Variations

Let’s explore how changes in risk factors affect the premium:

- Accident History: If Alex had one accident in the past five years, the premium might increase by 25% to $700. Two accidents could result in an even higher premium.

- Higher-Risk Location: Moving to a higher-risk area could increase the premium by 10% or more, depending on the area’s accident and crime rates.

- Lower Deductible: Choosing a lower deductible, say $250, would likely increase the premium by around 5-10%, reflecting the increased financial responsibility for the insurer.

Summary

In conclusion, the decision to pay insurance premiums annually requires careful consideration of individual financial circumstances and risk tolerance. While annual payments often offer cost savings, they necessitate robust financial planning. By understanding the factors that determine premium amounts, exploring available payment methods, and utilizing available resources, individuals can effectively manage their insurance costs and ensure consistent coverage. The ultimate goal is a secure and financially sound approach to insurance protection.

FAQ Section

What happens if I miss an annual premium payment?

Missing an annual premium payment can lead to policy lapse or cancellation, resulting in a loss of coverage. Grace periods vary by insurer and policy, but contacting your insurer immediately is crucial to explore options for reinstatement.

Can I change my premium payment frequency after I’ve started paying annually?

Generally, yes. However, this may involve contacting your insurer and potentially incurring administrative fees or adjustments to your premium amount. The availability of changing payment frequencies depends on your policy and the insurer’s specific rules.

Are there tax benefits associated with paying insurance premiums annually?

Tax implications for insurance premiums vary by location and policy type. Some premiums might be tax-deductible, but this depends on individual circumstances and applicable tax laws. Consult a tax professional for personalized advice.